Summary

S&P 500 Index: First introduced on March 4, 1957 by Standard & Poor’s as a benchmark index for the U.S. stock market, it has become one of the most widely followed indicators of American equities. The index is composed of 500 large-cap companies listed on the New York Stock Exchange and the Nasdaq, covering roughly 80% of the total U.S. stock market capitalization, which makes it a practical proxy for the overall market. With globally influential companies such as Apple, Microsoft, Nvidia, Amazon, and Alphabet (Google) among its constituents, the S&P 500 is widely regarded as a barometer of the health of the U.S. economy rather than just a simple market index. Legendary investor Warren Buffett has expressed such strong conviction in a low-cost S&P 500 index fund that he directed in his will that 90% of his wife’s inheritance be invested in one, underscoring his belief in broad, long-term exposure to the U.S. stock market.

Types and Key Characteristics of Underlying Assets

S&P 500 is broadly diversified across 11 major sectors, with the approximate weightings shown below. Information Technology holds the largest share at around 30%, followed by Health Care at about 13%, Financials at roughly 11%, Consumer Discretionary at around 10%, and Communication Services at about 9%. The remaining sectors are Industrials (about 8%), Consumer Staples (around 6%), Energy (about 4%), Utilities (about 3%), Real Estate (around 2.5%), and Materials (around 2%). Although the top 10 companies account for roughly 35–40% of the index, the other 490 names provide broad diversification, helping to significantly reduce the impact of idiosyncratic risk from any single stock.

Performance: Key Historical Metrics

Over the past 10 years (November 2014 to November 2024), the S&P 500 has delivered the following investment performance. The annualized average return was 11.29%, representing a remarkably solid track record. The best annual return was 28.79% in 2021, while the worst was -19.95% in 2022. The cumulative 10-year return reached 187.24%, meaning an initial investment of 10 thousand USD would have grown to approximately 28.72 thousand USD.

The maximum drawdown (MDD) was -33.92% on March 23, 2020, and the recovery period was only about 148 days (roughly 4.9 months). This highlights how quickly the market bounced back even after the sharp COVID-19 crash. The Sharpe ratio came in at 0.4086 and the Sortino ratio at 0.4976, indicating a reasonably favorable level of risk-adjusted returns. Annualized volatility was 17.83%, which is a volatility profile well suited to long-term investing.

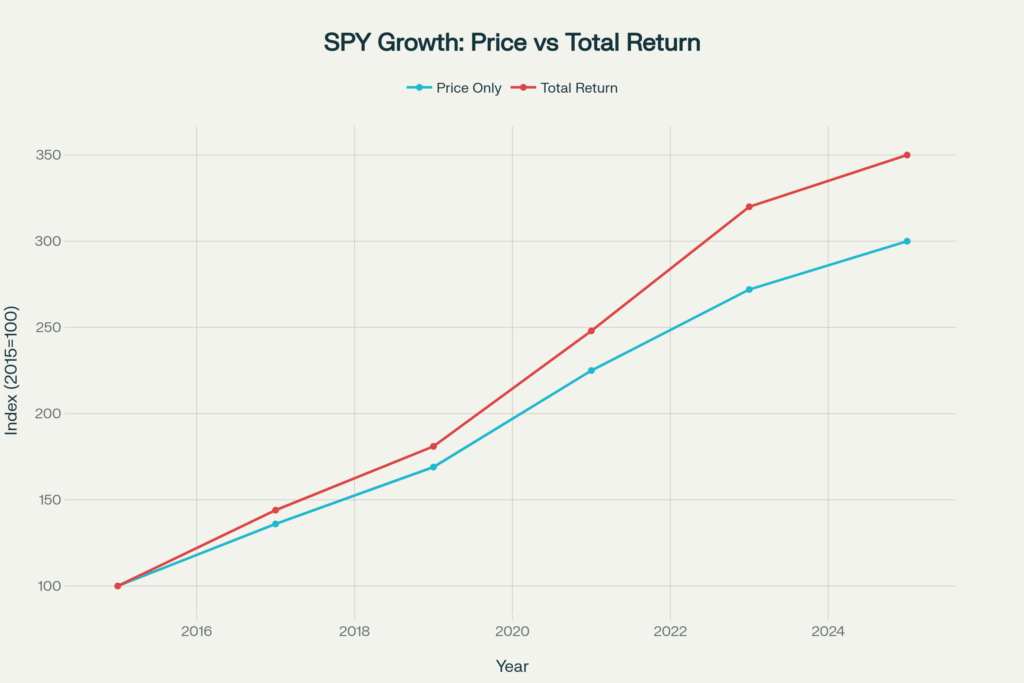

Dividend reinvestment further enhances returns. Over the past 10 years, the flagship S&P 500 ETF SPY has delivered an annualized return of around 11%, but when all dividends are reinvested, the annualized return improves to about 13%.

Investable U.S.-Listed and Korea-Listed ETFs

U.S.-Listed S&P 500 ETF

| Category | SPY | VOO | IVV | SPYM |

|---|---|---|---|---|

| Management company | State Street (SPDR) | Vanguard | BlackRock (iShares) | State Street (SPDR Portfolio) |

| Index | S&P 500 | S&P 500 | S&P 500 | S&P 500 |

| Expense Ratio | 0.09% | 0.03% | 0.03% | 0.02% (S&P 500 중 최저 수준) |

| Stock Price Level | The highest price in the $500 range | High-$400s | Mid‑$500 range | Around $60 |

| AUM | Very large, the first and flagship ETF | The largest S&P 500 ETFs available today | The next largest ETFs after SPY and VOO | Growing rapidly after the fee reduction, now at a mid-to-large scale. |

| Average trading volume and liquidity | Best among the four, making it ideal for both day trading and institutional trading. | High enough, but still lower than SPY. | Very solid, just one notch below SPY | Relatively low, but increased in recent years, sufficient for long‑term investing. |

| Dividend | Quarterly | Quarterly | Quarterly | Quarterly |

| Dividend yield | Around 1.2% | Around 1.2% | Around 1.2% | Around 1.2% |

| Structure and key characteristics | Listed in 1993 as the first S&P 500 ETF, it is heavily used for options and futures-linked trading, making it a preferred vehicle for institutional investors and short‑term traders. | A flagship ultra‑low‑cost ETF for long‑term investing, it is one of the most popular choices in retirement and pension accounts. | BlackRock’s core ETF has a very similar profile and performance to VOO. | SPDR’s lower‑fee S&P 500 version, designed for small, long‑term investors, with its ticker changed to SPYM from 2025 onward. |

| Summary of its key strengths | Top‑tier liquidity, making it one of the best ETFs for active trading. | Largest asset size combined with low fees, making it a “classic” core ETF for retirement investing. | A well‑balanced, all‑round choice with solid management, liquidity, and fees. | The lowest fee at 0.02% and a lower share price make it ideal for systematic investing and small long‑term contributions. |

In the U.S. market, the three main S&P 500 ETFs each come with their own characteristics. SPY (SPDR S&P 500 ETF Trust [finance:SPDR S&P 500 ETF Trust]) is the oldest and most well‑known option, with extremely high trading volume but a relatively higher expense ratio of 0.0945%. VOO (Vanguard S&P 500 ETF [finance:Vanguard S&P 500 ETF]) is managed by Vanguard and offers a low 0.03% expense ratio, making it one of the fastest‑growing products in recent years. IVV (iShares Core S&P 500 ETF [finance:iShares Core S&P 500 ETF]) is run by BlackRock under the iShares brand and also charges a low 0.03% fee. SPYM (State Street SPDR Portfolio S&P 500 ETF [finance:SPDR Portfolio S&P 500 ETF]) has the lowest fee at 0.02%, which makes it especially attractive for typical individual investors with smaller account sizes who prioritize minimizing costs over absolute fund size.

Korea‑listed S&P 500 ETFs

The main S&P 500 ETFs listed on the Korean stock market have the added benefit of being eligible for investment through retirement accounts. TIGER US S&P500 is managed by Mirae Asset and boasts the largest asset size of over 5 trillion KRW along with the highest trading volume. KODEX US S&P500 TR, run by Samsung Asset Management, offers the lowest expense ratio at 0.0099% and follows a total‑return structure that automatically reinvests dividends. ACE US S&P500 from Korea Investment Trust Management and RISE US S&P500 from KB Asset Management are also strong alternatives.

From a long‑term investor’s perspective, the choice largely comes down to how dividends are handled. If you want to automatically reinvest dividends and maximize the power of compounding, KODEX’s total‑return structure is more advantageous. If you prefer steady cash flow or want to use the dividends directly, the TIGER structure may be a better fit.

Diversification: Evaluating and Enhancing the Effectiveness of Your Investment Strategy

Advantages of diversification

One key advantage of investing solely in the S&P 500 is that your money is automatically spread across 500 companies, which makes the risk from any single stock extremely low. In addition, while roughly 85–90% of active funds fail to beat the market over time, an S&P 500 index approach reliably delivers the market’s average return.

There is still a clear need for diversification. Today, the top 10 companies make up roughly 35–40% of the S&P 500, and many investors view its tech exposure as excessively concentrated. In this context, adding global diversification can be a sensible way to reduce single‑market and sector risk, and allocating a portion of the portfolio to other asset classes such as bonds can also be a meaningful strategy for smoothing volatility and stabilizing long‑term returns.

Investment recommendations

For investors in their 20s and early 30s, allocating 100% to the S&P 500 can be highly effective. Over a 30‑year horizon, the power of compounding can realistically grow your capital by more than tenfold. For investors in their 40s and 50s, a more balanced mix such as 70% S&P 500 and 30% bonds is generally recommended to stabilize volatility while still participating in equity growth. If you want broader global diversification, you can complement U.S. equities with developed and emerging markets indexes. Especially from a long‑term asset‑allocation perspective, using a dollar‑cost averaging (DCA) approach—investing a fixed amount every month regardless of market conditions—tends to be a very effective way to build wealth steadily over time.